Swaap = HODL + AMM - IL

We build the pure market making protocol. No IL, only yields.

We envision a world where capital efficiency would be both simple and open to everyone, not just quants.

TL;DR: 0-impermanent loss, dynamic liquidity efficiency, built-in market risks coverage and multi-asset support.

Liquidity dilemma in traditional finance 🏊

Liquidity is a critical aspect of every market. It represents the ability to sell/buy assets with ease and at low costs. When liquidity is high it essentially means less risks and more efficiency for capital flows.

In traditional finance, providing liquidity is taken care of by market makers (MM) who act as buffers between sellers and buyers. Their role consists in continuously offering short and long positions to fill sell/buy orders that traders would eventually place. Thus offering a kind of “fluidity” or liquidity to the market.

Under its purest form, market making generates revenues solely from the intermediary role market makers play, and these latter avoid asset exposure risks at all cost. It means that they try to minimise the time to settle their long/short positions and hedge themselves against any potential risk of depreciation/appreciation of their securities at the same time.

The bid-ask spread — which corresponds to the difference between the sell and buy prices applied by the market makers — is the common answer to that dual problem and is optimized to be both market competitive as well as a form of insurance against market risks. This spread needs to be completely dynamic to be able to take into account the ever-changing conditions that markets usually display. Simply put, market makers charge low fees to drastically increase trading volumes and the overall revenue when market is safe, and apply higher fees when market becomes particularly wild to be able to maintain its operations at low risk, continue to earn fees and keep their capital safe from losses.

When done efficiently at scale it can be a rather profitable activity: Citadel Securities’s reported $6.7B in revenue gives us a powerful reminder of it. RobinHood Q2 2021 earnings call is another good illustration with a reported $451M in “transaction-based” revenue, as a payment for order flow (PFOF) — which corresponds only to a fraction of what its market maker partners earn.

Now, when looking at the centralized cryptocurrency market we can see that the same logic applies with Coinbase charging a dynamic spread based on market conditions for its asset swap service. It totally makes sense as, despite having different market conditions, the risk exposure remains.

The emergence of AMMs 🤖

As a decentralized alternative that embraces the security, transparency and efficiency of blockchain, Automated Market Maker (AMM) systems — first introduced in 2016 by Vitalik Buterin — quickly became popular, especially under the constant product form imagined by Uniswap and later on generalized by Balancer to multi-asset pools with arbitrary weightings.

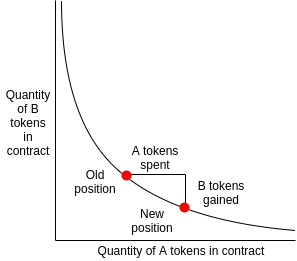

While it is able to provide a simple and elegant link between price, liquidity and efficiency (cf. fig.1), it fails to capture the market complexity.

This is mostly due to the fact that no usage of global market data (e.g. volatility, price, etc.) is made.

As a result, the system is static — which means not competitive and running high capital risks— and forced to address two rather different problems at the same time: market liquidity and price discovery.

While addressing the former can offer the same service than the one market maker provide in a traditional financial markets, addressing the latter one with the current AMM implementations (Uniswap, Balancer, etc.) corresponds to a continuous portfolio rebalancing and is equivalent to increase the pool’s risk exposure to poorly performing assets which directly translates into what has been called the “impermanent loss” (IL).

To put it in another perspective: investing in the popular BTC-ETH-stablecoin pool in 2015 in such AMMs would have led to an astonishing +90% loss in capital (fee collection excluded) compared to an HODL strategy.

And in this case, to only counterbalance the effect of impermanent loss you would have needed an APY of +100% every single year over this 6 years period 😞

Even a “top10 market cap. cryptos” pool would have lead to a +95% IL…!

Why do we need a better solution? 🤔

Today, the best investment vehicles in the whole blockchain landscape are the projects themselves, offering X00%+ CAGR over the past decade.

Basically, continuously selling highly performant assets — which traditional AMMs do— is usually not a good choice for non expert users as it will essentially translate to either:

- accept important impermanent losses

- setup a complex and real-time portfolio management policy

- invest in highly correlated asset pools to avoid IL

In other words, today’s DEXes’ users are facing a poor-performance / poor-UX / poor-risk-management dilemma.

On the other side, TradFi with the Index ETFs has seen a democratisation of investing by providing efficient, diversified, and passive investment products at the same time.

Index ETFs have indeed the appealing property of being a rather simple and passive investment vehicle allowing everyone with a capital to gain exposure to the growing economy, and have displayed better-than-hedge-fund performances in the last decade.

👋 the Matrix Market Maker

Swaap has been designed to solve this exact aforementioned dilemma.

First, it totally decouples the market-making from the price discovery by leveraging on-chain data from oracles such as Chainlink, removing de facto the impermanent loss.

Then, it provides adaptive market making fee regimes based on market conditions thanks to a stochastic approach. On the one hand, it is more competitive than traditional automated AMMs when the market is less risky. On the other hand, fees are increased to account for additional risk in volatile market conditions.

Finally, it handles multi-asset pools by design, thus allowing for a diversified and passive form of investing.

All those features come built-in in the Swaap DEX thanks to our new market maker system. We called it the Matrix Market Maker (MMM) and we discuss it in more details in our recently released whitepaper.

It is now possible for the first time to both a) invest in the best crypto projects as with HODL / Index ETFs strategies, while b) harvesting high yields for your liquidity — at the same time, in the same place, with minimal risk!

Join the community 🤗

Website: swaap.finance

Twitter: twitter.com/SwaapFinance

GitHub: github.com/swaap-labs

Whitepaper: swaap.finance/whitepaper.pdf